Have you ever dreamed of starting your own boutique, beauty parlour, tailoring business, grocery shop, food venture, or home-based enterprise but stopped because of a lack of money?

You’re certainly not alone. Across Gujarat, thousands of talented women have business ideas, practical skills, and the determination to succeed. However, arranging capital is often the biggest challenge. Traditional loans can involve high interest rates, collateral requirements, and complicated procedures that discourage many aspiring entrepreneurs from taking the first step.

This is exactly where the Chief Minister Women’s Upliftment Scheme makes a meaningful difference. Designed specifically to support women entrepreneurs, this initiative aims to provide affordable financial assistance, entrepreneurship support, and skill development opportunities. The scheme encourages women to establish new businesses or strengthen existing enterprises without worrying about heavy interest burdens or collateral requirements.

What makes this program particularly attractive is its focus on economic empowerment. Rather than offering temporary assistance, the scheme helps women create sustainable income sources that can support their families and contribute to local economic growth. Whether you’re a first-time entrepreneur or someone looking to expand a small business, understanding this scheme could open doors to opportunities that might otherwise seem out of reach.

Understanding the Chief Minister Women’s Upliftment Scheme and Its Purpose

The Chief Minister Women’s Upliftment Scheme, commonly associated with women entrepreneurship promotion in Gujarat, was introduced with a simple yet powerful objective: helping women become financially independent through self-employment and business ownership. The government recognized that many women possess valuable skills and business ideas but often lack access to affordable financing. By removing financial barriers, the scheme aims to encourage women to participate more actively in economic activities and entrepreneurship.

What many people overlook is that entrepreneurship does more than generate income for one individual. When a woman successfully starts and grows a business, the positive effects often extend to her family and community. Small businesses frequently create additional employment opportunities, support local suppliers, and contribute to regional economic development. This broader impact is one of the reasons why governments increasingly invest in women-focused entrepreneurship programs.

Another important aspect of the scheme is its emphasis on long-term sustainability rather than short-term financial aid. Instead of simply distributing funds, the initiative promotes responsible business development through financial support combined with skill enhancement opportunities. This approach increases the likelihood that businesses will survive and grow beyond their initial stages.

The scheme also reflects a larger shift toward encouraging women to become job creators instead of solely job seekers. In recent years, Gujarat has witnessed growing participation of women in sectors such as retail, food processing, beauty services, handicrafts, tailoring, digital services, and home-based manufacturing. Programs like this help accelerate that trend by providing easier access to funding.

Key Features That Make the Scheme Attractive

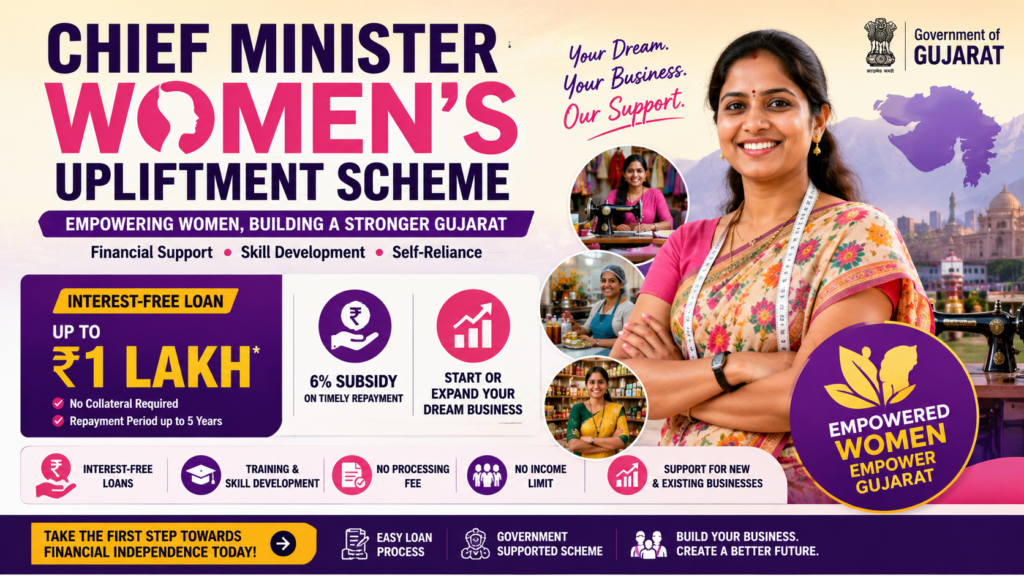

One of the strongest features of the scheme is the availability of interest-free loans of up to ₹1 lakh. For many small entrepreneurs, interest payments can become a major financial burden during the early stages of business development. By eliminating interest costs, the scheme allows women to focus on business growth rather than worrying about increasing loan liabilities.

Equally important is the absence of collateral requirements. Traditional lenders often ask borrowers to pledge property, assets, or other forms of security. Many aspiring women entrepreneurs may not possess such assets in their own names. Under this scheme, eligible applicants can access financial support without the challenge of arranging collateral security.

Another valuable benefit is the extended repayment period. Borrowers generally receive sufficient time to repay the loan, often stretching up to five years. This flexibility helps businesses stabilize before facing significant repayment pressure. For small enterprises, especially those operating in competitive markets, manageable repayment schedules can significantly improve survival rates.

The government also encourages responsible borrowing behavior through loan repayment incentives. Women who repay their loans on time may become eligible for additional benefits or subsidy-related support, making timely repayment financially rewarding.

Eligibility Criteria, Benefits, and Financial Assistance Available

Before applying, it’s important to understand who can benefit from the scheme. Eligibility requirements are designed to ensure that assistance reaches genuine women entrepreneurs who intend to establish or expand viable businesses within Gujarat.

Applicants must generally be women residents of Gujarat and should have attained adulthood. Basic educational qualifications are also required. The scheme typically expects applicants to have completed at least the eighth standard. This educational requirement helps ensure that beneficiaries can manage business records, understand loan documentation, and participate effectively in training programs.

Unlike some welfare programs that impose strict income restrictions, this scheme is notable because it remains accessible to women from different economic backgrounds. This wider accessibility allows aspiring entrepreneurs from diverse social and financial circumstances to participate and benefit.

The financial assistance available under the scheme can support numerous business categories. Women can use the loan amount to establish or expand ventures such as tailoring units, beauty parlours, food processing businesses, handicraft enterprises, retail stores, coaching centers, home-based manufacturing operations, and service-oriented businesses. The flexibility in business selection allows applicants to pursue opportunities aligned with their skills and market demand.

How the Financial Benefits Can Help a Small Business

Imagine a woman who has excellent tailoring skills but lacks funds to purchase sewing machines, fabric inventory, and basic shop infrastructure. A loan obtained under the scheme can provide the initial capital needed to start operations. Instead of waiting years to save enough money, she can begin earning sooner and gradually expand her customer base.

Similarly, a woman interested in opening a beauty parlour may require funds for equipment, furniture, cosmetics, and basic renovation work. The availability of an interest-free loan significantly reduces the cost of entering the market. Since there is no collateral requirement, she doesn’t need to risk family property or assets to pursue her entrepreneurial goals.

I’ve noticed that many successful small businesses begin with surprisingly modest investments. What often matters more than large capital is the ability to access funding at the right time. The Chief Minister Women’s Upliftment Scheme addresses exactly that challenge by providing timely financial support to eligible women entrepreneurs.

The scheme’s training and skill development components also deserve attention. Many new entrepreneurs underestimate the importance of business management skills. Understanding budgeting, customer service, marketing, inventory management, and basic accounting can significantly improve the chances of long-term success. Training programs offered through the scheme help bridge these knowledge gaps.

Documents Required Before Applying

Applicants should prepare all required documents carefully before submitting their applications. Proper documentation not only speeds up the approval process but also reduces the likelihood of application rejection due to incomplete information.

Generally required documents include Aadhaar Card, government-issued identity proof, address proof, educational qualification certificates, recent passport-sized photographs, and bank account details. Applicants are also expected to provide a detailed business plan outlining the proposed venture, estimated investment requirements, operational strategy, and expected revenue generation.

Many first-time applicants view business plans as complicated documents. In reality, a business plan simply explains what business you intend to start, how you plan to operate it, how much money is needed, and how you expect the venture to generate income. A well-prepared plan demonstrates seriousness and improves credibility during evaluation.

Application Process, Important Considerations, and Practical Tips

The application process is designed to be relatively straightforward, but careful preparation remains essential. Interested applicants should obtain the prescribed application form through the appropriate official channels and complete it accurately. All information provided should match the supporting documents submitted with the application.

Once the application form is completed, applicants should attach all required documents and submit them to the designated authority. Authorities review applications to verify eligibility, assess business proposals, and ensure compliance with scheme guidelines. Successful applicants may then proceed through the remaining approval and loan processing stages.

One mistake I’ve seen many aspiring entrepreneurs make is rushing through the application process without carefully reviewing their business plans. A strong proposal should clearly explain the market opportunity, customer demand, expected expenses, and potential earnings. The more realistic and well-organized the proposal, the better the chances of creating a positive impression.

Another important consideration involves financial discipline after receiving the loan. While obtaining funding is an important milestone, business success ultimately depends on how effectively the money is utilized. Borrowers should avoid diverting funds toward non-business expenses and instead focus on activities that directly contribute to business growth and revenue generation.

The scheme excludes certain categories of applicants. Government employees generally cannot avail themselves of the benefits, and applicants receiving similar benefits under specific other programs may face restrictions. Understanding these conditions beforehand can help avoid unnecessary delays and disappointment during the application process.

Frequently Asked Questions

Can the loan be used for any type of business?

The scheme is intended to support legitimate and viable business ventures that contribute to self-employment and entrepreneurship. Applicants should present a realistic business proposal that demonstrates potential sustainability and income generation. Authorities may evaluate the feasibility of the proposed venture before approving financial assistance.

Is there any income limit for women applying under the scheme?

One of the attractive aspects of this program is its broader accessibility. Unlike certain welfare schemes that target only specific income groups, the Chief Minister Women’s Upliftment Scheme generally does not impose a strict income ceiling. This allows women from various financial backgrounds to pursue entrepreneurial opportunities.

Is collateral security required to obtain the loan?

No. The scheme is designed to reduce barriers for aspiring women entrepreneurs. Eligible applicants can access financial assistance without pledging property or other assets as collateral, making it easier for women with limited resources to participate.

Do applicants need an existing business to apply?

Not necessarily. The scheme supports both new business ventures and expansion of existing enterprises. Women with well-planned startup ideas can apply, provided they meet the eligibility requirements and submit a convincing business proposal.

Is preparing a business plan mandatory?

Yes, a business plan is typically an important part of the application process. It helps authorities understand the nature of the proposed business, estimated investment requirements, revenue expectations, and long-term viability. A detailed and realistic plan can strengthen the application significantly.

Final Thoughts

The Chief Minister Women’s Upliftment Scheme represents much more than a financial assistance program. It serves as a practical tool for empowering women through entrepreneurship, self-employment, and economic participation. By offering interest-free business loans, eliminating collateral requirements, and supporting skill development, the scheme creates opportunities that might otherwise remain inaccessible for many aspiring entrepreneurs.

For women who have been waiting for the right moment to start a business, this initiative can provide both the confidence and resources needed to take that first step. Whether your dream involves opening a boutique, launching a food business, establishing a beauty parlour, or creating a home-based enterprise, the scheme offers a pathway toward financial independence and long-term growth.

Success in entrepreneurship rarely happens overnight. However, with proper planning, responsible financial management, and a commitment to learning, the support provided under this scheme can help transform a simple business idea into a sustainable and rewarding venture. For many women across Gujarat, that journey toward self-reliance may begin with a single application.